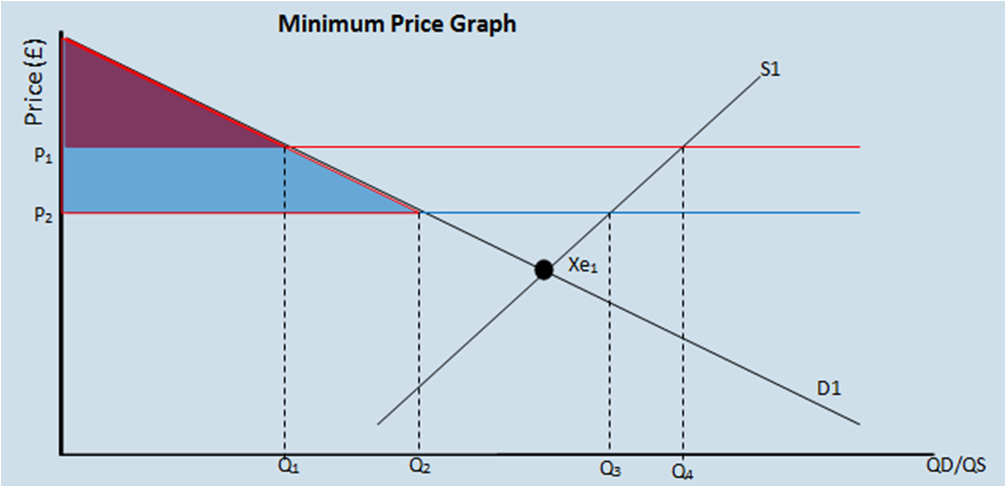

The red line represents P1 which is the initial minimum price, and the blue line represents the new minimum price (P2). The red triangle shows the initial consumer surplus and the blue triangle shows the new increase consumer surplus.

From the graph above we can see that both the initial and the new minimum prices are both above the natural equilibrium of Xe1 which means the new price is artificial. At P1 only Q1 was demanded but because supply was at Q4 the government had to buy the rest of the supply (Q4 – Q1) at the price of P1.

At the new price (P2) quantity demanded is increased (an extension in the demand curve) due to the reduced price. This means that demand is now at Q2 but supply is at Q3 so the government still has to buy back the rest of the supply (Q3 – Q2) at the price of P2. This represents a decrease in government expenditure by moving the minimum price from P1 to P2. Because there is a minimum price in place, suppliers would try to produce as much as possible as they can reliably estimate their revenue.

Advantages and Disadvantages of a Minimum Price Scheme

Advantages include a reduction of commodity price fluctuations making it easier for consumers to budget their spending, supplier incomes are stabilised (and increased) leading to increased investment in their respected industry. Employment is maintained in the industries and supply of agricultural commodities is guaranteed even in times of poor harvest due to surplus stockpiles.

Disadvantages include the price of food increasing, the opportunity cost of government spending meaning it cant be spent elsewhere. Excess supply represents an inefficient allocation of resources and suppliers are guaranteed an income which may cause them to become less efficient. Also there are storage and security costs associated with stockpiling, perishable goods may have to be destroyed and some surpluses may be sold in overseas markets at very low prices effectively destroying local producers in these countries.